[论文解读] Pricing Cryptocurrency Options

本论文评估具有跳跃的仿射随机波动性(SVCJ)、SVJ,以及 Burstein–Ricci(BR)风格模型,用于比特币和加密货币指数定价欧洲期权,采用贝叶斯估计和蒙特卡洛仿真,修订聚焦于基于SV的模型和鲁棒性。

Cryptocurrencies, especially Bitcoin (BTC), which comprise a new digital asset class, have drawn extraordinary worldwide attention. The characteristics of the cryptocurrency/BTC include a high level of speculation, extreme volatility and price discontinuity. We propose a pricing mechanism based on a stochastic volatility with a correlated jump (SVCJ) model and compare it to a flexible co-jump model by Bandi and Renò (2016). The estimation results of both models confirm the impact of jumps and co-jumps on options obtained via simulation and an analysis of the implied volatility curve. We show that a sizeable proportion of price jumps are significantly and contemporaneously anti-correlated with jumps in volatility. Our study comprises pioneering research on pricing BTC options. We show how the proposed pricing mechanism underlines the importance of jumps in cryptocurrency markets.

研究动机与目标

- 在跳跃和随机波动性存在的背景下,推动对加密货币期权的定价研究。

- 比较 BTC 和 CRIX 动态下的仿射跳扩散模型(SVCJ、SVJ、BR)。

- 通过基于仿真的方法评估模型拟合度及对期权定价的含义。

- 提供数据来源、鲁棒性检验,以及面向机构解读结果的指南。

提出的方法

- 在贝叶斯框架下估计 BTC 与 CRIX 动态,使用 SVCJ、SVJ 与 BR 模型。

- 将模型校准至价格路径,并通过蒙特卡洛仿真计算欧洲期权价值。

- 使用拟合优度指标和诊断图(如 MSE、QQ 图)比较模型。

- 评估期权价格对模型选择和参数取值的敏感性。

- 记录数据来源并提供代码可用性参考(Quantlets)。

实验结果

研究问题

- RQ1仿射跳扩散模型(SVCJ、SVJ、BR)是否比其他模型更好地捕捉 Bitcoin 和 CRIX 的价格动态?

- RQ2不同模型如何影响欧洲加密货币期权的定价?

- RQ3结果对数据来源和估计选择(如初始值与先验)有多大鲁棒性?

- RQ4在这些模型下,实证隐含波动率表面是否能对 Bitcoin 和 CRIX 呈现市场化的偏斜?

主要发现

- 在所报告的诊断中,SVCJ 模型通常比 SVJ 提供更好的拟合(更低的 MSE)。

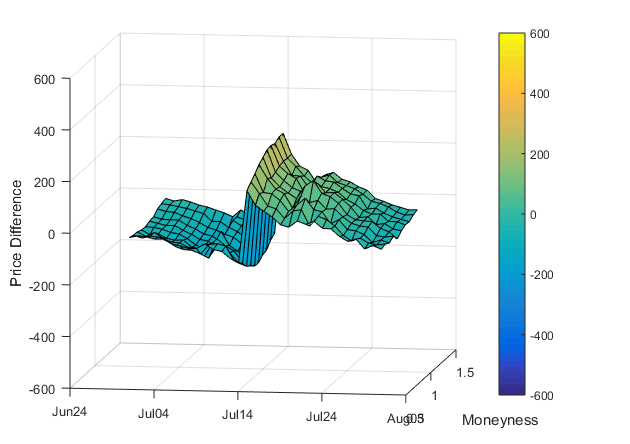

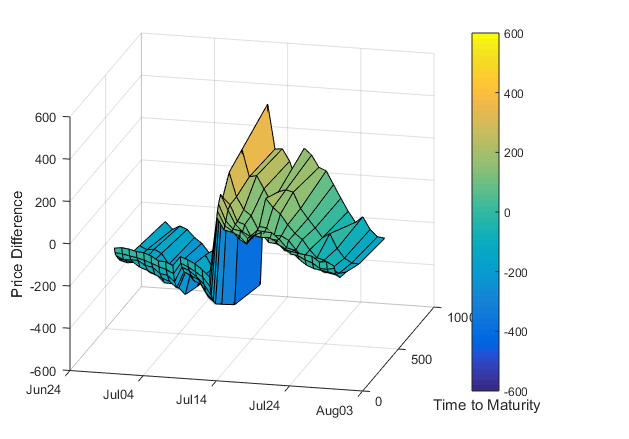

- 在 SVCJ 和 BR 模型下生成的期权价格在实值/虚值和到期时间上的表现具有特定规律,揭示隐含波动率表面的曲率。

- 作者提供了便于复制的数据与代码生态(Quantlets),并强调带参数不确定性的贝叶斯估计。

- 鲁棒性步骤包括将 ARIMA 和 GARCH 组件移至附录,并聚焦于对期权定价相关的基于 SV 的动态。

- 在各修订版本中,讨论并将比特币动态与更广泛的加密指数之间的相关性置于机构使用的语境中(如 CRIX 与 BTC)。

更好的研究,从现在开始

从论文设计到论文写作,大幅缩短您的研究时间。

无需绑定信用卡

本解读由 AI 生成,并经人工编辑审核。