[論文レビュー] From Factor Models to Deep Learning: Machine Learning in Reshaping Empirical Asset Pricing

機械学習とAIが経験的資産価格設定を再構築する方法の総合的レビュー。伝統的なファクターモデルからMLベースの予測、最適化、マルチモーダルデータ統合まで。

This paper comprehensively reviews the application of machine learning (ML) and AI in finance, specifically in the context of asset pricing. It starts by summarizing the traditional asset pricing models and examining their limitations in capturing the complexities of financial markets. It explores how 1) ML models, including supervised, unsupervised, semi-supervised, and reinforcement learning, provide versatile frameworks to address these complexities, and 2) the incorporation of advanced ML algorithms into traditional financial models enhances return prediction and portfolio optimization. These methods can adapt to changing market dynamics by modeling structural changes and incorporating heterogeneous data sources, such as text and images. In addition, this paper explores challenges in applying ML in asset pricing, addressing the growing demand for explainability in decision-making and mitigating overfitting in complex models. This paper aims to provide insights into novel methodologies showcasing the potential of ML to reshape the future of quantitative finance.

研究の動機と目的

- 従来の資産価格設定モデルの限界と柔軟でデータ駆動型アプローチの必要性を評価する。

- ML手法(教師あり、教師なし、半教師あり、強化学習)が予測精度とデータヘテロゲネティをどう扱うかを調査する。

- MLで強化されたポートフォリオ最適化とリスク管理を検討する。

- 説明可能性、過適合、データ品質、規制上の考慮事項などの課題を強調し、将来の方向性を概説する。

提案手法

- 伝統的な資産価格設定フレームワークとその限界をレビューする。

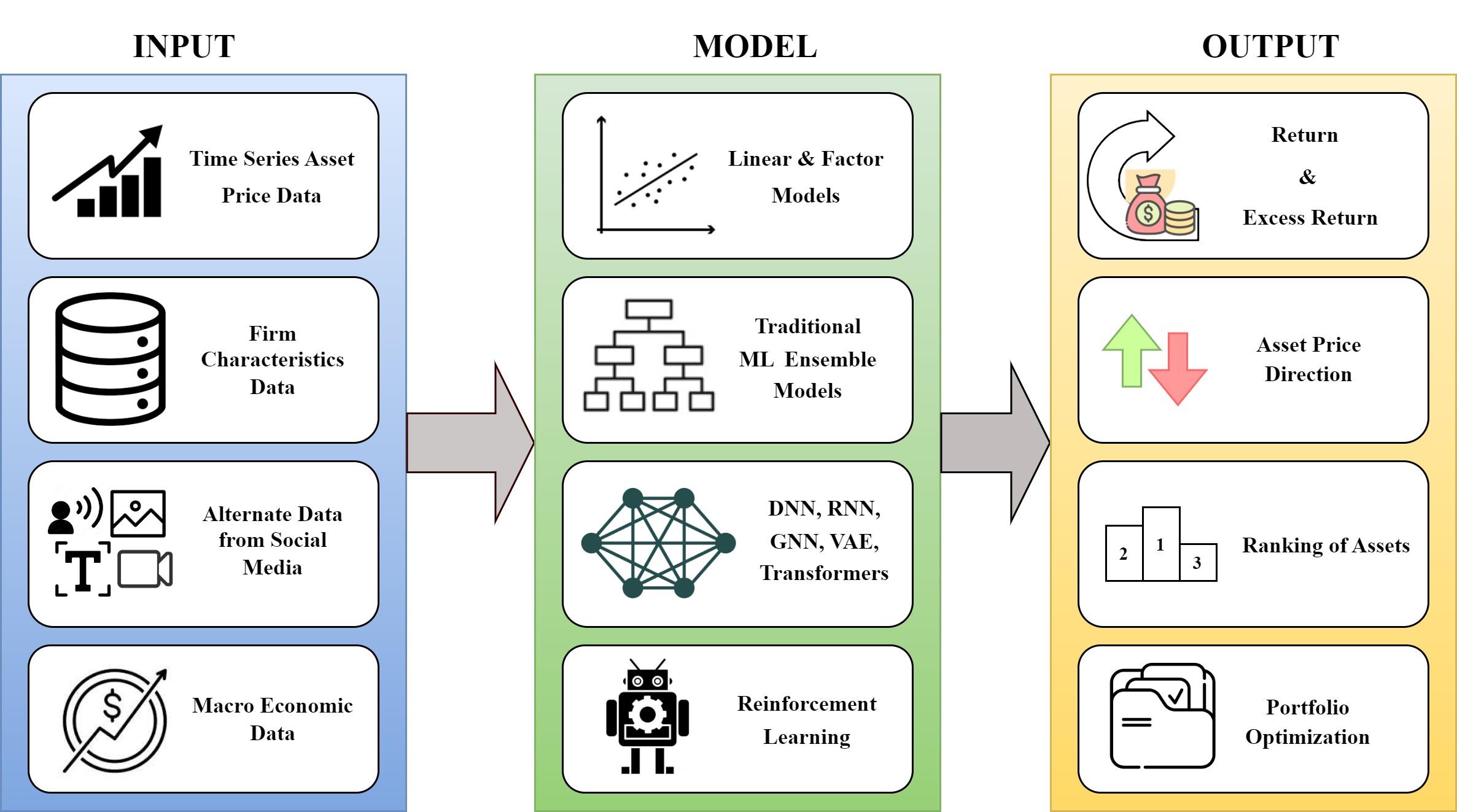

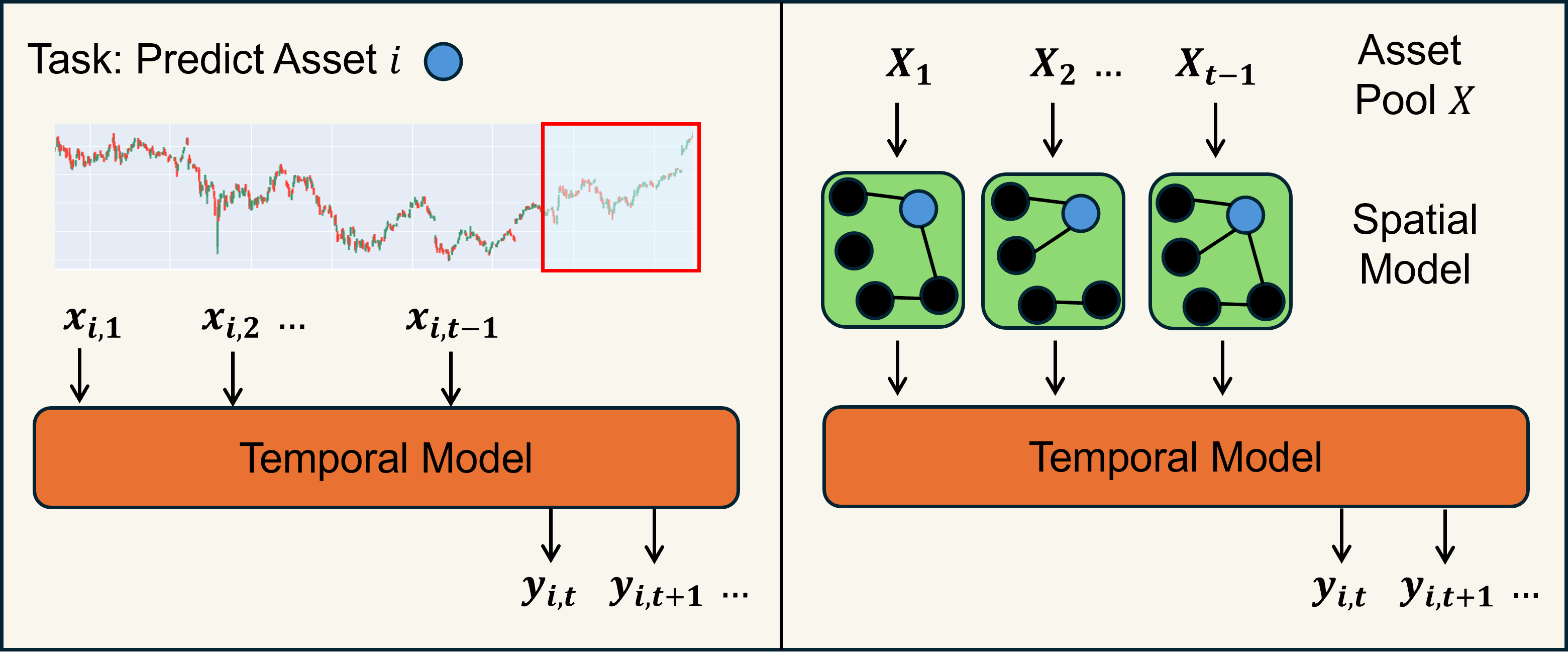

- 資産価格設定タスクにMLファミリをマッピングする(予測、ランキング、最適化)。

- グラフ/トランスフォーマーを含む資産価格設定の時系列および時空間MLモデルを説明する。

- 次元削減、欠損データ補完、代替データの組み込みについて論じる。

- MLベースの資産価格設定における課題と将来の方向性を検討する。

実験結果

リサーチクエスチョン

- RQ1MLアプローチは従来のファクターモデルを超えて資産リスクプレミアの推定をどう改善するか?

- RQ2資産価格設定において時系列・横断的ダイナミクスを最も適切に捉えるMLアーキテクチャは何か(グラフやトランスフォーマーを含む)?

- RQ3MLは経験的金融におけるポートフォリオ最適化とリスク管理をどう強化できるか?

- RQ4主な課題(過適合、解釈性、データ品質、規制)とMLベース資産価格設定での緩和方法は何か?

- RQ5資産価格設定へのML統合で最も有望な将来の研究方向は何か?

主な発見

- MLとAIは、非線形性をモデル化し、資産価格設定に異種データを組み込む柔軟な枠組みを提供する。

- MLの進歩は予測、ランキング、ポートフォリオ最適化を含み、グラフベースの手法を含む時系列・時空間モデルがある。

- 次元削減と欠損データの補完手法はファクターゾウ問題と欠測データを緩和し、安定性と解釈性を向上させる。

- 代替データ(テキスト、画像、音声)の組込みはマルチモーダルモデルを通じて価格形成の洞察を強化し、トランスフォーマーと深層学習の進展に支えられている。

- 著者は過適合、解釈性、データ入手、規制遵守、オンライン/適応学習フレームワークの必要性などの課題を議論している。

より良い研究を、今すぐ始めましょう

論文設計から論文執筆まで、研究時間を劇的に削減しましょう。

クレジットカード登録不要

このレビューはAIが作成し、人間の編集者が確認しました。