[論文レビュー] The Inflation Attention Threshold and Inflation Surges

この論文は、インフレ注視閾値を導入し、インフレが約4%を超えるとエージェントがインフレに対する注意を高め、 regimeごとの注視水準を推定し、この閾値がフィリップス曲線に非線形ダイナミクスを生み出すとともに、金融政策への意味ある影響を示す。校正は米国のインフレ急上昇のダイナミクスを再現し、テイラー規則下の福利損失は注意閾値が有効なときに大きくなることを示唆する。

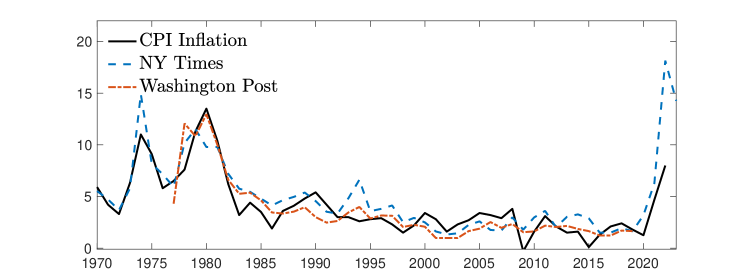

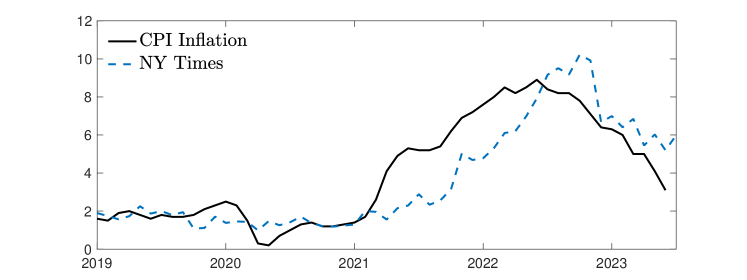

At the outbreak of the recent inflation surge, the public's attention to inflation was low but increased quickly once inflation started to rise. In this paper, I quantify when and by how much the public's attention to inflation changes, and derive the macroeconomic implications of these attention changes. I estimate an attention threshold at an inflation rate of about $4%$, and that attention doubles when inflation exceeds this threshold. Adverse supply shocks become more inflationary in times of high attention, and the increase in people's attention to inflation in 2021 accounts for half of the subsequent supply-driven inflation. I develop a model accounting for the attention threshold and show that shocks that are usually short lived lead to a persistent surge in inflation if they induce an increase in people's attention. The attention threshold further lengthens the last mile of disinflation after an inflation surge, and leads to an asymmetry in the dynamics of inflation.

研究の動機と目的

- インフレへの注視がインフレ動学と政策にとってなぜ重要か動機づける。

- 長期にわたる調査データからインフレ注視閾値と regimeごとの注視水準を推定する。

- この閾値をニューニューヨーク型モデルに組み込み、非線形なフィリップス曲線のダイナミクスを導出する。

- 最近の急上昇時のインフレとインフレ期待に合わせて米国データでモデルを較正する。

- 注視主導のインフレ動学の下での金融政策の規範的含意を評価する。

提案手法

- 動的カルマンフィルタ風の期待形成モデルにおける閾値回帰を用いて注視水準を推定する。

- 遅行インフレが推定閾値を超えたときに注視が regime を切り替えることを許容する。

- 二つの regime ごとの注視パラメータ(低・高)と閾値を二乗残差を最小化して推定する。

- 限定的な注視と regime-switching 注視メカニズムを備えたニュー・ケインジアン模型を較正する。

- 注視閾値あり/なし、理性的期待と比較してモデルのダイナミクスを比較する。

- 単純なテイラー型金融政策ルールの下での福利影響を評価する。

実験結果

リサーチクエスチョン

- RQ1調査データで観測されたインフレ注視閾値はいくらと推定されるか?

- RQ2低インフレ・高インフレの regime で注視水準はどう異なるか?

- RQ3ニューニューヨーク型枠組みでインフレ注視閾値を導入すると、インフレとインフレ期待のダイナミクスにどう影響するか?

- RQ4注視が regime に依存する場合の福利と金融政策への含意は何か?

- RQ5実証結果は最近の米国のインフレ急増のダイナミクスと一致しているか?

主な発見

| 閾値 barπ | 低注視 γπ,L | 高注視 γπ,H | p値 γπ,L=γπ,H | |

|---|---|---|---|---|

| 平均期待値 | 3.98% | 0.18 | 0.36 | 0.000 |

| 中央値の期待値 | 4.41% | 0.16 | 0.23 | 0.000 |

| 四半期頻度 | 3.21% | 0.14 | 0.38 | 0.000 |

- 推定された注視閾値は 3.98%(平均期待)で、仕様により 3.63–4.41%。

- 低注視 γπ,L ≈ 0.18;高注視 γπ,H ≈ 0.36(平均/全体仕様); 高注視 regime で注視が倍になる。

- 閾値超えはフィリップス曲線と総需要に非線形な増幅をもたらし、注視が上がるとインフレを強化する。

- 較正されたモデルは、最近の急増時に米国で観察された山型のインフレ動態と進化する期待を再現する。

- テイラー型政策に類似した政策は、注視閾値モデルの下で理性的期待や完全に情報があるモデルより福利損失が大きくなる。

- 高インフレ期間には注意が高く、インフレ報道はインフレが高いほど増え、注意効果を強化する。

より良い研究を、今すぐ始めましょう

論文設計から論文執筆まで、研究時間を劇的に削減しましょう。

クレジットカード登録不要

このレビューはAIが作成し、人間の編集者が確認しました。